Apply for Citigold

Apply for Citigold Citi Wealth Perspectives

Citi Wealth Perspectives Citi Plus

Citi Plus Digital Banking

Digital Banking Apply for International Banking Account

Apply for International Banking Account Citibank Debit Mastercard

Citibank Debit Mastercard Activate your Citibank Debit Mastercard

Activate your Citibank Debit Mastercard Our Wealth Philosophy

Our Wealth Philosophy Citi FX Calculator

Citi FX Calculator Get Travel Insurance Quote

Get Travel Insurance Quote Apply for Citi Credit Card

Apply for Citi Credit Card Citi PayAll

Citi PayAll Card Services

Card Services Manage Your Credit Application

Manage Your Credit Application Refer a friend to Citi Credit Card

Refer a friend to Citi Credit Card Manage Your Mortgage Application

Manage Your Mortgage Application

Singapore Quarter 3, 2024

Momentum building

Rekindling growth

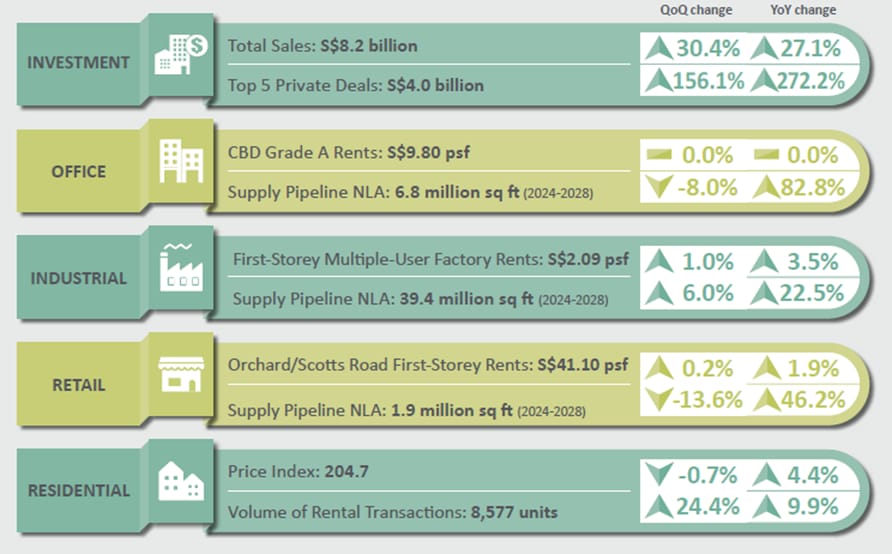

3Q 2024 AT A GLANCE

KEY HIGHLIGHTS

Residential

Residential property price index fell 0.7% q-o-q, attributed by the landed segment which witnessed a 3.4% decline q-o-q. Rental rates found its footing, rising 0.8% after declining for three consecutive quarters.

Investment

Singapore’s investment sales reached S$8.2 billion, fuelled by strong developer activity in Government Land Sales and key acquisitions by REITs. However, some investors continue to adopt a cautious stance in anticipation of the interest rate cuts by the Federal Reserve.

Retail

In 3Q 2024, island-wide occupancy rate increased to 93.5% from 93.4% in 2Q 2024. Rental rates in the Orchard/Scotts Road and Fringe/Suburban areas saw a 0.3% rise q-o-q, while Other City Areas remained stable.

Office

In 3Q 2024, Singapore’s central region office rental index declined marginally by 0.5% q-o-q, while overall occupancy rates dipped slightly to 94.5%. The increase in shadow spaces indicates an ongoing market adjustment on the back of tenants’ shift in preference towards smaller and more efficient office units.

ECONOMY

KEY INDICATORS

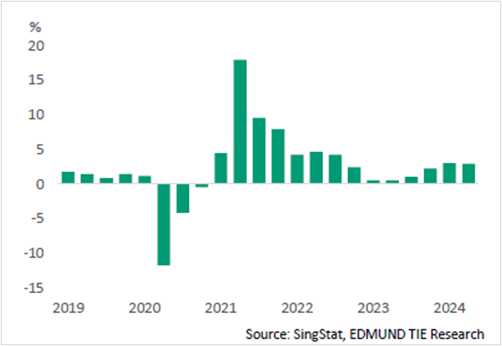

GDP Growth

Singapore’s economy grew by 4.1% y-o-y in 3Q 2024, extending the 2.9% growth in 2Q 2024. Monetary Authority of Singapore expects GDP to hit the upper end of the 2% to 3% forecast in 2024.

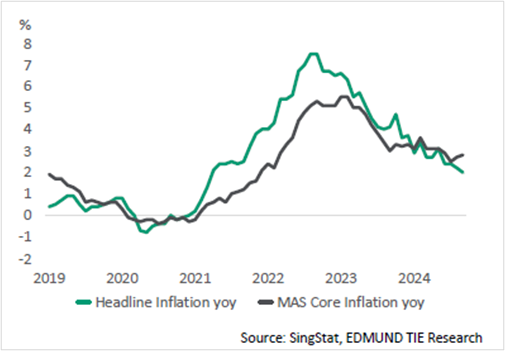

Inflation

Core inflation recorded a low of 2.5% y-o-y in July 2024 before rising to 2.8% y-o-y in September 2024. The rise in inflation was largely due to retail and other goods. According to MAS and MTI, overall inflation is expected at 2.5% for the whole of 2024.

Non-oil Domestic Exports

Non-Oil Domestic Exports (3MMA y-o-y) witnessed positive growth of 9.7% q-o-q for 3Q 2024. Total export for both electronics and non-electronics sectors grew in 3Q 2024, recording a q-o-q increase of 10.6% and 9.0% respectively.

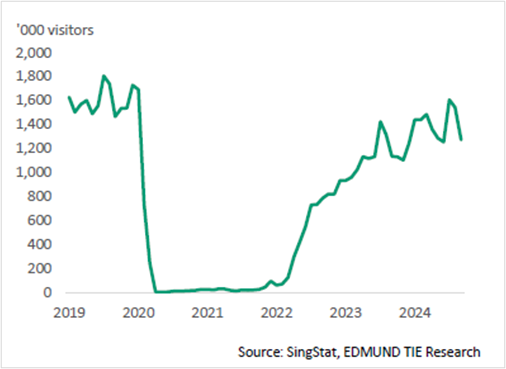

International Visitor Arrivals

International Visitor Arrivals (IVA) reached 1.29 million in September 2024, down 17.5% from 1.54 million recorded in August 2024. Despite the recent decline, IVA is trending to pre-COVID19 levels of 1.59 million in 2019. Year-todate, IVA totals 12.65 million, moving towards STB’s 2024 forecast of 15 to 16.5 million visitors.

INVESTMENT

Investment market fuelled by strategic acquisitions in 3Q 2024

KEY HIGHLIGHTS

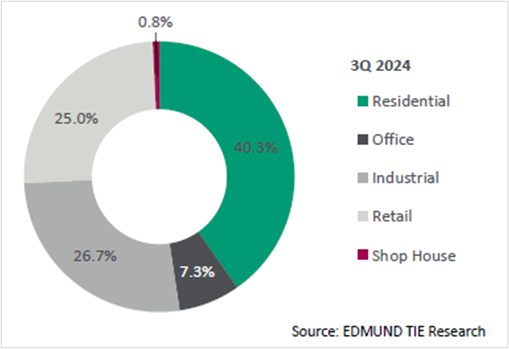

Investment Sales Sectorial Contribution (%)

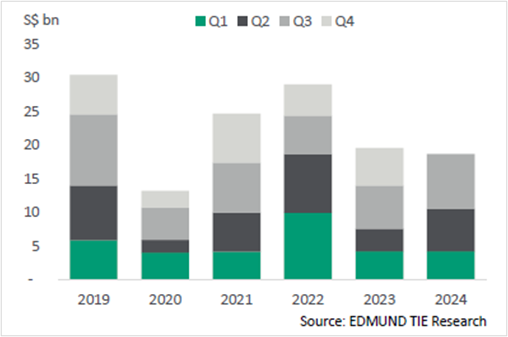

Investment Sales (S$ billion)

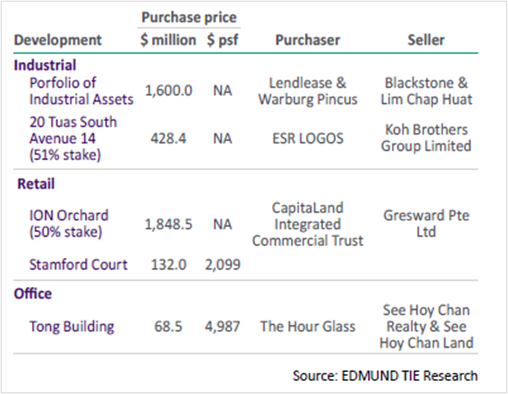

Top 5 Private Investment Sales 2Q 2024 (S$ million)

Market Commentary

- In 3Q 2024, total investment sales in Singapore reached S$8.2 billion, a 30.2% q-o-q increase from S$6.3 billion in 2Q 2024.

- Five Government Land Sales (GLS) sites were awarded within the quarter, notably Canberra Crescent, De Souza Avenue, Margaret Drive, Zion Road (Parcel B) and Jalan Loyang Besar Executive Condominium (EC) totalling S$2.34 billion. The strong developer participation in GLS tenders has led to competitive bidding, supporting the residential sector as the largest contributor to investment sales in 3Q 2024. However, the Jurong Lake District and Media Circle sites received bids that were assessed to be too low, resulting in those two parcels not being awarded.

- In the private sector, significant acquisitions underscore strategic investment trends. CapitaLand acquired a 50% stake in ION Orchard, reinforcing its position in prime retail assets and aligning with the retail sector recovery. Lendlease expanded its portfolio by acquiring several industrial properties, reflecting the rising demand for logistic and warehousing supported by the continued growth in e-commerce.

- Investor interest in land and property acquisition remained robust, fueled by an expected interest rate cut by the Federal Reserve in September. However, some investors adopted a more cautious approach, delaying investment decisions as negative yield spread still persist for some sectors. This mix of optimism and caution illustrates the evolving sentiment in the market, as stakeholders navigate potential changes in economic conditions.

Market Outlook

- The GLS market is expected to maintain steady activity through the rest of the year. In 3Q 2024, the Urban Redevelopment Authority (URA) and Housing Development Board (HDB) released two sites amid ongoing economy recovery, with these sites expected to close and be awarded in the fourth quarter of 2024. However, investors will remain focused on identifying opportunities as a part of their investment strategies.

- Developer’s discerning approach to acquisitions suggests that future growth may be moderate, influenced by ongoing economic and market uncertainties.

RESIDENTIAL

Residential price index declines

KEY HIGHLIGHTS

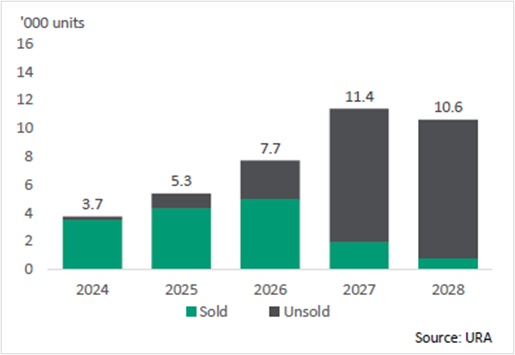

Residential Supply Pipeline

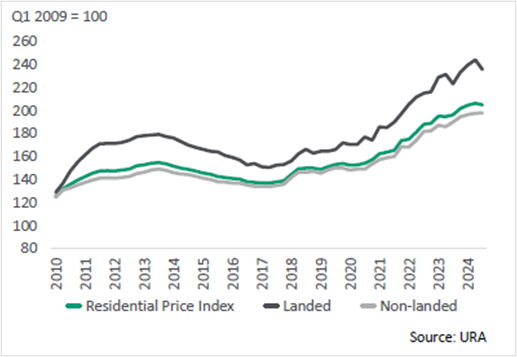

Property Price Index

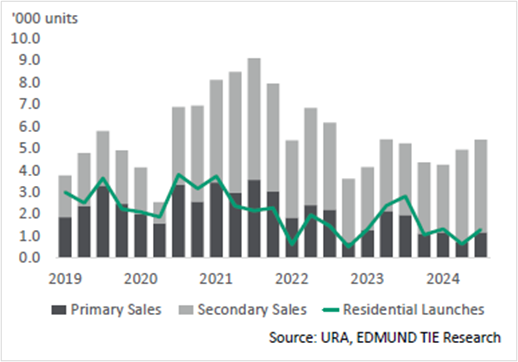

Residential Sales and Launch Volume

Market Commentary

- In 3Q 2024, the residential price index fell 0.7% q-o-q, offsetting the 0.9% growth from 2Q 2024. The landed segment saw a decline of 3.4% q-o-q, counteracting the 1.9% q-o-q growth in 2Q 2024. Meanwhile, the non-landed segment rose marginally by 0.1% q-o-q, extending the 0.6% growth from 2Q 2024..

- The marginal increase of 0.1% q-o-q in the non-landed segment was a result of the RCR segment witnessing 0.8% q-o-q growth, albeit the CCR segment declining 1.1% q-o-q. The OCR segment prices plateaued in 3Q 2024.

- The overall price decline in 3Q 2024 can be attributed to buyers seeking out more affordable condominiums and competitively priced new suburban units compared to other markets.

- Transaction volume rose 2.2% in 3Q 2024 to 5,372 units, recording a rise in both primary and secondary sales. Primary sales transactions rose to 1,160 units in 3Q 2024, from 725 units in 2Q 2024. This is in tandem with more new units launched in 3Q 2024 compared to 2Q 2024, 1,284 units and 635 units, respectively. Correspondingly Secondary sales transaction volumes rose marginally 0.5% to 4,212 units in 3Q 2024 from 4,190 units in 2Q 2024.

- Foreign purchases continue to remain low at 43 units sold, or 0.8% of total transactions. Of which, 27 transactions were purchased by US, Swiss or Norwegian nationals, who are eligible for the ABSD remissions under the Free Trade Agreements (FTAs).

- In the rental market, rental rates have broken its three consecutive quarters of decline streak with a 0.8% q-o-q rise in 3Q 2024. The rise in rental prices was supported by the uptick in rental transactions in 3Q 2024. 25,731 rental transactions were recorded in 3Q 2024, up 24.4% from the 20,676 transactions recorded in 2Q 2024.

Market Outlook

- For 4Q 2024, we expect primary sales transactions to rise, attributed to positive take-up rates in several new launch projects at record price levels. These will be reflected in the residential property price index for 4Q 2024.

- Residential rental rates are expected remain stable as landlords and tenants bridge pricing expectations.

RETAIL

Overall retail performance remains steady

KEY HIGHLIGHTS

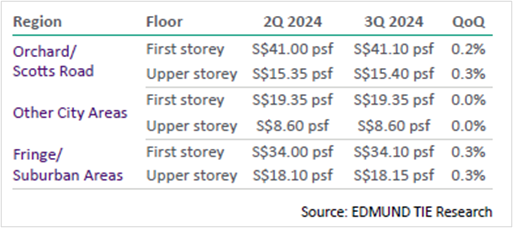

Retail Prime Rental Rents

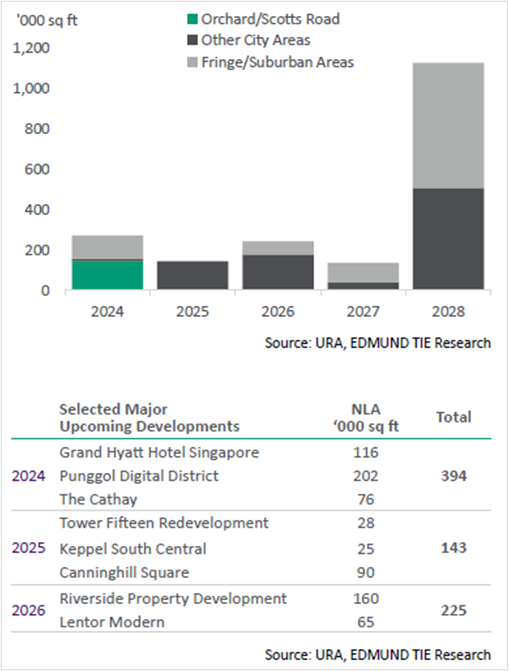

Retail Supply Pipeline (NLA)

Market Commentary

- The rise in international visitor arrivals to 4.4 million in the quarter from the 3.9 million recorded in 3Q 2023, reflects a strong recovery in Singapore’s tourism sector. Factors driving this growth include increased global travel confidence, major events, and enhanced airline connectivity.

- In 3Q 2024, occupancy rates island-wide increased to 93.5% from 93.4% in 2Q 2024, particularly in the central area retail spaces. Orchard/Scotts Road occupancy rate experienced a slight q-o-q increase to 93.0% from 92.9% in 2Q 2024, while the Other City Area increased to 92.2% from 91.8%, respectively. Albeit, Fringe/Suburban Area saw a marginal q-o-q decrease of 0.1 percentage points from 94.1% to 94.0%, indicative of healthy demand in the suburban retail sector.

- In 3Q 2024, prime first-storey rental rates along Orchard/Scotts Road rose by 0.3%, reaching S$ 41.10 psf, driven by strong demand despite on-going challenges in the Fringe/Suburban retail markets where rental rates increased to S$34.10 psf. Other City Areas remained stable at S$ 19.35 psf.

- The reopening of Tampines 1 in the Outside Central Region (OCR) captures a significant share of retail space in this quarter. This development is set to influence competitive dynamics and consumer expectations, potentially driving innovation and growth in the sector.

Market Outlook

- Prime retail rents are expected to experience sustained growth, due to limited pipeline of upcoming retail supply, steady domestic demand and a rise in international visitor arrivals. As tourism rebounds, demand for retail and MICE experiences, particularly in prime locations, is expected to strengthen.

OFFICE

Stable growth amid shifting tenant dynamics

KEY HIGHLIGHTS

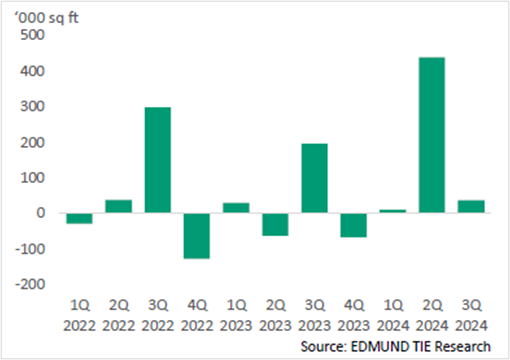

CBD Premium and Grade A Office Net Absorption

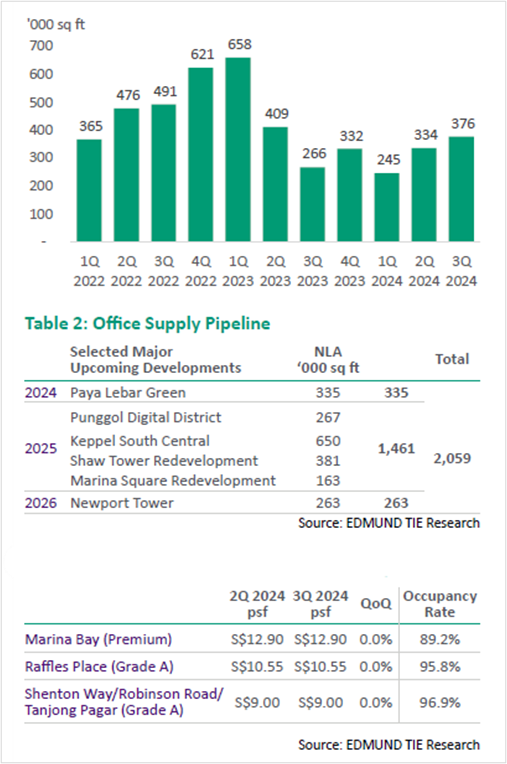

Shadow Space (NLA) and Office Supply Pipeline

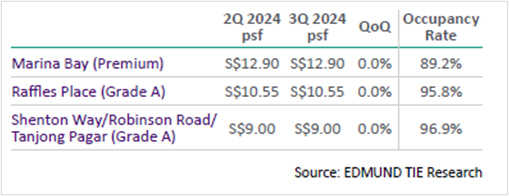

Average Office Rents and Occupancy Rates

Market Commentary

- In 3Q 2024, Singapore’s central region rental index remained stable, declining marginally by 0.5% q-o-q. Rental rates underscore resilience amidst new completions and market fluctuations.

- Island-wide occupancy rates dipped slightly to 94.5%, while both CBD and Non-CBD areas saw a marginal increase of 0.1%. In contrast, decentralised areas experienced a 1.3% decline in occupancy, primarily due to the completion of Labrador Tower that added approximately 0.7 million sq ft of office space in the Alexandra area, achieving 70% commitment at Temporary Occupancy Permit (TOP).

- Overall net absorption of office space across Singapore reached 417,000 sq ft in 3Q 2024, with the CBD and non-CBD areas contributing 20,000 sq ft and 17,000 sq ft, respectively. In the decentralised areas, net absorption was recorded at 380,000 sq ft due to the completion of Labrador Towers.

- Shadow spaces increased to 376,000 sq ft, indicative of ongoing adjustments by tenants in upcoming lease renewals.

- A notable shift in tenant preferences has emerged, with a growing demand for smaller, more efficient office units, reflecting a strategic focus on optimising space and managing costs. It has been observed that majority of the new office leases stemmed from lease renewals.

- Noteworthy leasing activity in the quarter included Datadog’s new office in South Beach Towers, Star Alliance’s relocation to One George Street, and IOI Central Boulevard Towers attracting high-profile multinational corporations such as Linklaters, Freshfields, Allied World Assurance, and Edrington.

Market Outlook

- Looking ahead, the recent completion of new developments is expected to create new opportunities for tenant to explore occupancy strategies.

- With only Paya Lebar Green set for completion in 2024, overall supply remains limited. Without any significant demand drivers, rental rates are expected to remain stable throughout the year. We expect downward pressure on rental rates for office spaces in non-central locations with limited accessibility and connectivity.

GENERAL DISCLOSURE

DISCLAIMER - EDMUND TIE & COMPANY

This report should not be relied upon as a basis for entering into transactions without seeking specific, qualified, professional advice. Whilst facts have been rigorously checked, Edmund Tie & Company can take no responsibility for any damage or loss suffered as a result of any inadvertent inaccuracy within this report. Information contained herein should not, in whole or part, be published, reproduced or referred to without prior approval. Any such reproduction should be credited to Edmund Tie & Company.

© Edmund Tie & Company 2024

Source: Edmund Tie & Company. Reproduced with permission.

Citibank Disclaimers and Important Notices

DISCLAIMER – CITIBANK

The market data and information herein contained (“Information”) is the product or service of a third party not affiliated to Citibank Singapore Limited (“CSL”) or its related entities. None of the Information represent the opinion of, counsel from, recommendation or endorsement by CSL, its related entities and their respective officers, employees, directors and agents (collectively, the “CSL Group”).

The Information is provided for general information and/or educational purposes only. No part of the Information may be reproduced without the prior written permission of CSL.

NO WARRANTY

The Information is provided “as is”, without warranty of any kind, it has not been independently verified by CSL Group and use of the Information is at your sole risk. The CSL Group shall not be liable and expressly disclaim liability for any error or omission in the content of the Information, or for any actions taken by you or any third party, in reliance thereon. The Information is not guaranteed to be error-free, or to be relied upon for investment purposes, and the CSL Group makes no representation or warranty as to the accuracy, truth, adequacy, timeliness or completeness, fitness for purpose, title, non infringement of third party rights or continued availability of the information.

LIMITATION OF LIABILITY

To the maximum extent permitted by law, the CSL Group shall not be liable for any loss or damage of any kind whatsoever (including, without limitation, any special, consequential, incidental or indirect damages, or damages for loss of profits, business interruption, and any and all forms of loss or damage, regardless of the form of action or the basis of the claim, whether or not foreseeable) arising out of the use of the information (provided in any medium), even if any member of the CSL Group, has been advised of the possibility of such loss or damage.

© 2024 CITIBANK

CITIBANK IS A REGISTERED SERVICE MARK OF CITIGROUP INC. OR CITIBANK, N.A.

CITIBANK SINGAPORE LIMITED. CO REG. NO. 200309485K