Apply for Citigold

Apply for Citigold Citi Wealth Perspectives

Citi Wealth Perspectives Citi Plus

Citi Plus Digital Banking

Digital Banking Apply for International Banking Account

Apply for International Banking Account Citibank Debit Mastercard

Citibank Debit Mastercard Activate your Citibank Debit Mastercard

Activate your Citibank Debit Mastercard Our Wealth Philosophy

Our Wealth Philosophy Citi FX Calculator

Citi FX Calculator Get Travel Insurance Quote

Get Travel Insurance Quote Apply for Citi Credit Card

Apply for Citi Credit Card Citi PayAll

Citi PayAll Card Services

Card Services Manage Your Credit Application

Manage Your Credit Application Refer a friend to Citi Credit Card

Refer a friend to Citi Credit Card Manage Your Mortgage Application

Manage Your Mortgage Application

Singapore Quarter 4, 2022

Market commentary

Shifting gears; positive momentum remains.

ECONOMY

Headwinds and uncertainties remain elevated

KEY HIGHLIGHTS

GROSS DOMESTIC PRODUCT (GDP)

FIXED ASSET INVESTMENTS (FAI)

UNEMPLOYMENT RATE

CONSUMER PRICE INDEX (CORE INFLATION)

Market Commentary

- Based on advance estimates, Singapore’s economy expanded by 2.2% y-o-y in Q4 2022, easing from the previous quarter’s 4.2% growth. Growth during the quarter was led by the expansion of the construction sector while the manufacturing sector contracted.

- Overall estimated economic growth for 2022 was 3.8%, half of 2021’s 7.6% growth, but slightly higher than the MTI’s forecast of 3.5%.

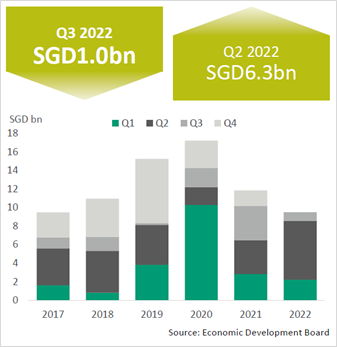

- Amid weaker economic sentiment, Singapore’s secured investment commitments totalled around SGD1bn in Q3 2022, a significant drop from SGD6.3bn in the previous quarter. The services sector was the main contributor to the quarter’s FAI (57%).

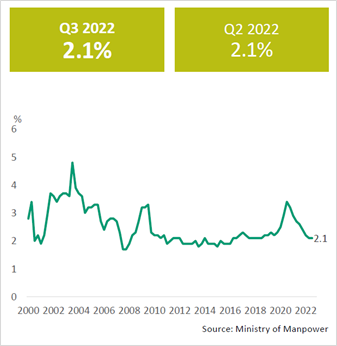

- The labour market remained tight in Q3 2022. The unemployment rate remained at near pre-pandemic levels and recorded 2.1% in Q3 2022, unchanged from the previous quarter Total employment continued its growth momentum (83,100) in Q3 2022, outpacing the previous quarter’s growth (71,100), led by improvements in the services sector (+40,600). On the other hand, the uptick in retrenchments was mainly derived from technology firms.

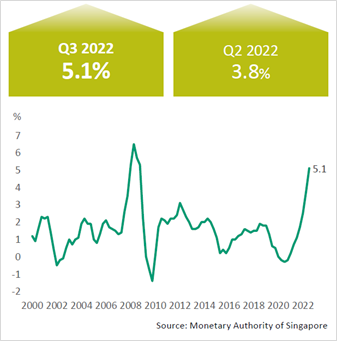

- Core inflation hit 5.1% in Q3 2022, though it was unchanged in November and eased discernibly in October from previous months’ decade-high levels. Prices of energy and food commodities stayed elevated amid ongoing supply constraints, while domestic wage pressures remained strong amid the tight labour market.

- Overall business sentiments for October 2022 to March 2023 remain negative in the manufacturing sector, amid protracted supply chain challenges, operational cost pressures and weaker macroeconomic conditions.

- Similarly, the services industry was also less upbeat on their outlook, though most industries expect business conditions to still improve for the October to March period due to increased tourism arrivals, events and the anticipated boost from the year-end festive season.

Market Outlook

- While aviation-and tourism-related as well as consumer-facing sectors will benefit from the travel recovery, the growth of export-oriented sectors such as electronics and chemicals clusters may be weighed down by the weaker external conditions.

- In 2023, the US and Eurozone are expected to experience sharp slowdowns while the global supply chain disruptions may persist amid the protracted Russia-Ukraine war.

- A further slowdown in Singapore’s economy is expected in 2023, with growth forecasted to be “between 0.5 and 2.5%” due to weakening global economic conditions.

- There are early indications of easing momentum in the labour market and improvements could slow over the next few quarters. While overall employment growth is expected to remain robust, growth could be uneven across sectors. Higher employment growth is anticipated for tourism-related sectors while outward-facing sectors may witness subdued growth amid the macroeconomic challenges.

- The MAS expects core inflation to be “around 4.0%” for 2022 and “3.5 to 4.5%” in 2023. Upside risks include fresh shocks to global commodity prices and more persistent-than-expected external inflation.

INVESTMENT

Higher rates limit transaction activity

KEY HIGHLIGHTS

INVESTMENT SALES (SGD billion)

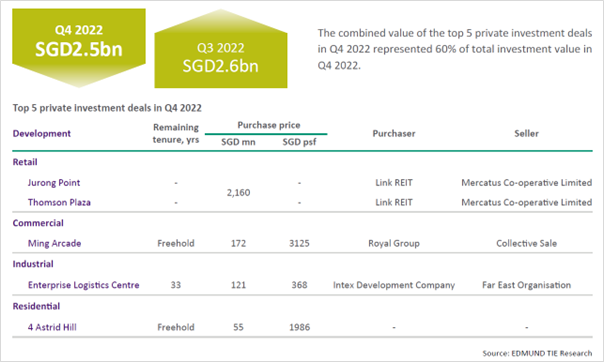

VALUE OF TOP 5 PRIVATE INVESTMENT DEALS (SGD billion)

Market Commentary

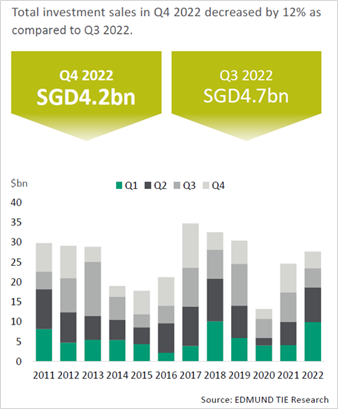

- Total investment sales reached SGD27.6bn in 2022, a 12% increase from the SGD24.6bn in 2021. This was despite a slowdown in investment activity in Q4 2022, which stood at SGD4.2bn, a 12% decrease from Q3 2022’s total investment sales of SGD4.7bn.

- Given the persistent interest rate hikes over the second half of 2022, coupled with new property cooling measures introduced at the end of Q3 2022, investors were more cautious in their investments decisions especially in the midst of economic uncertainties that will continue into the new year. In Q4 2022, the sale of land parcels under the Government Land Sales (GLS) programme contributed significantly to the total investment sales for the quarter. The total investment sales for the quarter was supported by the collective sales market as well with the sale of Jurong Point and Swing By @ Thomson Plaza that closed towards the end of the quarter as the largest deal in 2022.

- The retail sector led the investment sales in the quarter, contributing SGD2.4bn (56%), followed by the residential sector contributing SGD1.2bn (28%). The retail investment sales for the quarter were largely due to the sale of Jurong Point and Swing By @Thomson Plaza at SGD2.2bn, recorded as the largest sale in 2022.

- The public investment sales market recorded around SGD0.5bn from the Government Land Sales (GLS) Programme, comprising two residential sites, at Bukit Timah Link and Hillview Rise.

- Bidding activity in early November for the launched Bukit Timah Hill and Hillview Rise sites was moderate with lower than usual number of bids for both sites. Developers were more cautious and strategic in their bids considering the current market conditions, especially with the tender closing a month after the recent announcement of property cooling measures.

- The collective sales market saw activity over the quarter, despite the latest cooling measures, with project launches and relaunches as well as the sale of Ming Arcade in December.

Market Outlook

- RESIDENTIAL: In 2023, the residential market will continue to see interest in areas with opportunities for transformation with the new MRT lines that allow for better connectivity, increasing the attractiveness and liveability of many neighbourhoods. With economic headwinds, inflation, and the persisting rounds of interest rate hikes, alongside the upcoming property tax hikes, developers will likely remain cautious with the expectation of a soft market climate and consumers tightening their spending given the increases in the cost of living.

- COMMERCIAL: With more countries lifting travel restrictions towards the end of 2022 and likely continuing into 2023, tourism and retail sectors expect greater recovery in 2023. As such, investors are likely to be more attracted to hospitality and retail assets especially with the pent-up demand for travel amongst both leisure and business travellers.

- RETAIL: Retail has seen changes in consumer preferences in their ideal shopping experience. The changes have allowed a greater flexibility in creating different in-store shopping experiences for their consumers. In turn, coupled with the recovery in the retail sector, the rejuvenation of the retail experience across many brands will likely attract investors towards the retail sector.

- OFFICE: The office market will continue to see consistent leasing demand supported by co-working operators and family offices, as well as the tight supply of quality office spaces in both the prime areas and in decentralised areas. In decentralised areas, quality office spaces will see leasing demand from firms as such spaces are in closer proximity to business activities away from the CBD. However, for investors, the low yields amid high borrowing costs will limit the investment appetite for larger deals.

- INDUSTRIAL: Singapore’s strong reputation for high-value manufacturing and R&D innovation will continue to attract investments, especially in modern warehouse and logistic spaces as e-commerce remains pivotal and corporates strengthen supply chains.

RESIDENTIAL

Economic headwinds to moderate price growth

KEY HIGHLIGHTS

PROPERTY PRICE INDEX OF ALL PRIVATE RESIDENTIAL PROPERTIES

PRIMARY AND SECONDARY SALES TRANSACTION VOLUME

RESIDENTIAL PIPELINE SUPPLY

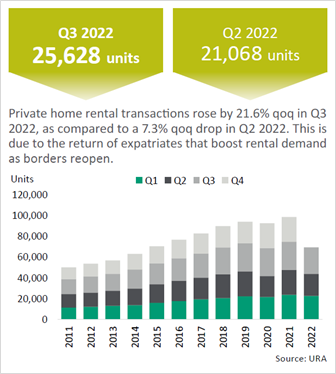

PRIVATE HOME RENTAL TRANSACTIONS

Market Commentary

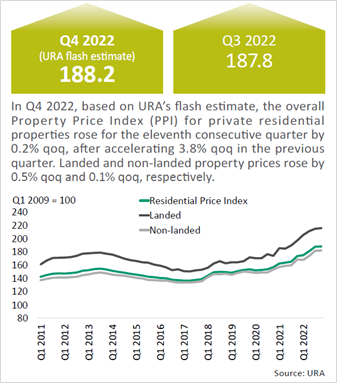

- In Q4 2022, based on URA’s flash estimate, the overall Property Price Index (PPI) for private residential properties rose for the eleventh consecutive quarter by 0.2% q-o-q, after accelerating 3.8% q-o-q in the previous quarter. Landed and non-landed property prices rose by 0.5% q-o-q and 0.1% q-o-q, respectively. There were five project launches in Q4 2022 – 3 project launches in the CCR and 2 project launches in the OCR.

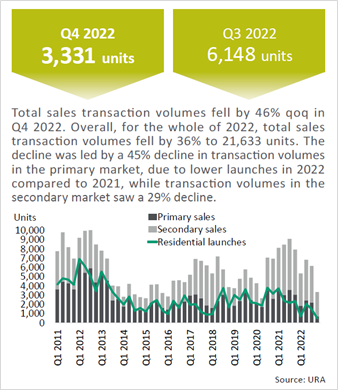

- Total sales transaction volumes fell by 46% q-o-q in Q4 2022. Overall, for the whole of 2022, total sales transaction volumes fell by 36% to 21,633 units. The decline was led by a 45% fall in transaction volumes in the primary market, due to fewer launches in 2022 compared to 2021, while transaction volumes in the secondary market saw a 29% decline.

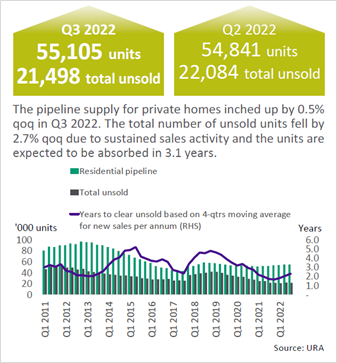

- The pipeline supply for private homes inched up by 0.5% q-o-q in Q3 2022. The total number of unsold units fell by 2.7% q-o-q due to sustained sales activity and the units are expected to be absorbed in 3.1 years.

- Private home rental transactions rose by 21.6% q-o-q in Q3 2022, as compared to a 7.3% q-o-q drop in Q2 2022, due to the return of expatriates that boost rental demand as borders reopen.

Market Outlook

- The government ramped up the confirmed list supply for the first half of 2023 to 4,090 units, the highest since the H1 2014 release. As more new homes are expected to be completed this year, this would likely alleviate the pressure on the tight rental market, moderating the pace of rental growth in 2023.

- Demand will continue to be largely supported by local first-time home buyers. Based on HDB’s flash estimate for Q4 2022, the public housing resale price rose by 2.1% q-o-q in Q4 2022, for the eleventh consecutive quarter. The strong public resale market in 2022 may provide tailwinds for upgrader demand for private homes in 2023.

- Overall, total primary sales volumes clocked about 7,100 units in 2022, down from 13,027 in 2021. This is on the back of rising interest rates and macro headwinds. Nonetheless, the overall property market is supported by strong household balance sheets and a tight labour market.

- Considering the economic and geopolitical headwinds as well as rising interest rates, property prices could moderate to 1-3% growth for 2023 from 2022’s 8.4% in 2022.

- Overall transaction activity is likely to see a slight moderation in 2023, with the secondary market bearing the brunt. Secondary sales volume is expected to reach between 10,000 and 12,000 units in 2023, down from 14,500 units for 2022, due to tighter financing conditions and rising interest rate that will weigh on housing affordability. Primary sales volume is expected to between 8,000 and 9,000 units in 2023, up from about 7,100 units for 2022, as a result of the surge in project launches in 2023.

RETAIL

Orchard retail spaces to outperform as tourism outlook brightens

KEY HIGHLIGHTS

AVERAGE RETAIL RENTAL (SGD/sq ft)

SUPPLY OF RETAIL SPACES (SQ M)

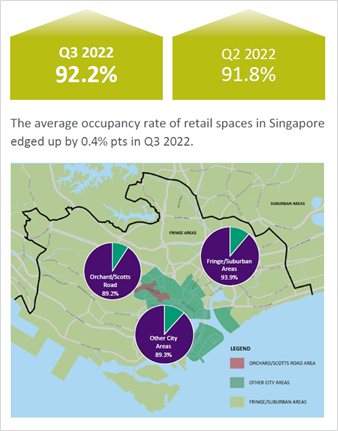

RETAIL OCCUPANCY RATES

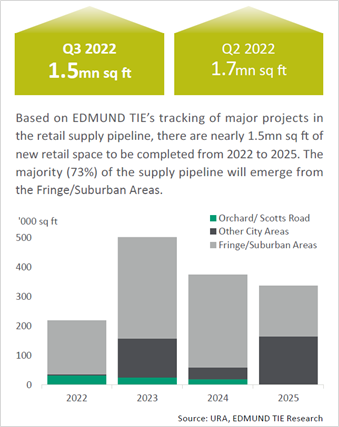

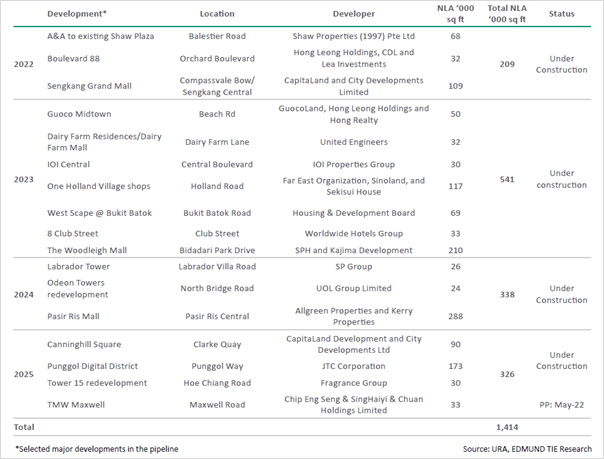

SUPPLY OF RETAIL SPACES (2022-2025) (sq ft)

The majority of the upcoming pipeline is the enhancement of existing malls and ancillary retail spaces at new hotel developments and mixed-use office buildings.

Market Commentary

- Overall retail demand continued to strengthen for the second consecutive quarter. In Q3 2022, the island-wide net absorption recorded 323,000 sq ft, a four-fold increase from 86,000 sq ft registered in the previous quarter. The pick-up in demand was largely broad-based across all segments, except for Fringe Area which recorded a negative take-up. The further easing of community and border measures that occurred in end-August, such as the removal of legal requirement for mask-wearing in most settings and the seven-day SHN requirement for all non-fully vaccinated incoming travellers, have contributed to the further recovery of the retail market.

- With demand outpacing supply, the overall occupancy rate edged up by 0.4 percentage points in Q3 2022 to 92.2% from 91.8% in the previous quarter, and it was the highest level recorded since Q4 2019. Among the various subzones, the Orchard/Scotts Road recorded the greatest improvement in occupancies due to buoyant leasing demand.

- Supported by the steadfast tourism recovery, prime first-storey spaces at Orchard/Scotts Road outperformed and recorded around 2.0% q-o-q rental growth in Q4 2022, compared to 1.0% q-o-q and 1.5% q-o-q rental growth for prime first-storey spaces at Other City Areas and Fringe/Suburban Areas respectively. For the whole of 2022, the Orchard/Scotts Road spaces (prime first-storey) witnessed the strongest rental growth of 7.4%, followed by Fringe/Suburban area (prime first-storey) at 6.7% and Other City Areas (prime first-storey) at 3.7%.

- Various new-to-market brands continued to establish a foothold in the local retail scene, including Anglo-French luxury fragrance house Creed at Raffles City, Café Kitsune (by French-Japanese lifestyle brand Maison Kitsune) at Capitol Singapore, South Korean convenience store chain Emart24 at Jurong Point and Nex, and Melbourne-based Puzzle Coffee at Ion Orchard. Brand expansions such as Levi’s at Ion Orchard (replaced La Senza), Uniqlo and Pedro at Raffles City, Eggslut’s second outlet at Suntec City and Don Don Donki at Jewel Changi Airport coincided with the year-end festive season. Recent pop-ups include the Prada Paradoxe pop-up at Paragon in October and online fashion blogshop Lovet’s first pop-up store at Jewel Changi Airport.

- On a 3-month moving average y-o-y basis, retail sales growth (excluding motor vehicles) declined to 13.2% as at November, from 18.6% in August. Year-to-date, retail sales grew by 10.8% y-o-y, compared with 11.1% for the whole of 2021. Retail sales for Wearing Apparel & Footwear, Food & Alcohol, Department Stores, and Watches & Jewellery recorded the greatest improvement y-o-y. Most of the retail trade categories experienced positive growth, except for Supermarkets & Hypermarkets, Mini-Marts & Convenience Stores and Motor Vehicles.

- Based on Q3 2022’s food and beverage services index, Food Caterers continued to register the largest improvement of 131.9% y-o-y due to higher demand for both event and in-flight catering with the easing of restrictions, followed by Restaurants which rose by 58.5%.

Market Outlook

- We expect the demand for retail space in 2023 to continue to strengthen with brightening prospects of the recovery of the retail sector. With the bulk of the supply pipeline (2022-2025) targeted to come onstream in 2023 (47%), which includes The Woodleigh Mall and One Holland Village shops, the supply-demand dynamics is expected to be balanced in 2023.

- The updated Retail Industry Transformation Map 2025, which focuses on local brands, innovation, talent, is anticipated to pave the way for innovation in the retail scene.

- Exciting transformations to the traditional physical retail landscape are also anticipated, as retailers continue to bring cohesion between the online retail experience and the in-store experience.

- However, we take caution that the considerable headwinds going forward due to uncertainties, such as high inflation, the re-emergence of new Covid variants, retightening of safety and border measures, may affect retail sentiment and consumer confidence. These uncertainties may reduce consumer spending and cap retail rental growth.

- In view of the significant cost pressures and headwinds, we expect sustained rental growth of between 7% and 9% for Orchard (prime first storey), as tourism recovery continues with the expectation of a further boost from China’s easing of measures. As for the other retail segments, we forecast rental growth of between 3% and 6% in 2023.

OFFICE

Greater completions and economic slowdown to moderate office market recovery

KEY HIGHLIGHTS

AVERAGE MONTHLY GROSS RENTS (SGD/sq ft)

SINGAPORE OFFICE SUPPLY (sq ft)

OCCUPANCY RATE OF PRIME CBD OFFICE SPACES

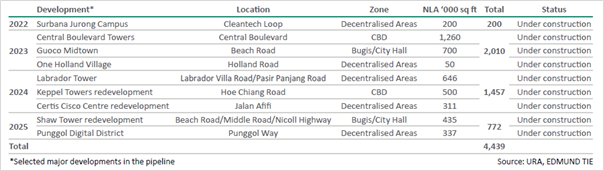

OFFICE SUPPLY PIPELINE (2022-2025) (sq ft)

Market Commentary

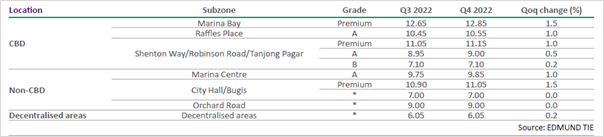

- Based on EDMUND TIE Research statistics, overall net absorption island-wide reversed from 410,848 sq ft in Q3 2022 to -126,248 sq ft in Q4 2022. Leasing demand for prime office spaces in Shenton Way/ Robinson Road/ Tanjong Pagar as well as in City Hall/Bugis areas saw growth in the quarter.

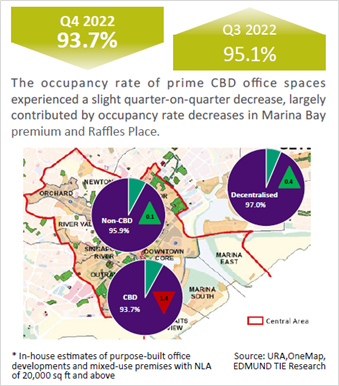

- In this quarter, occupancy rates in Marina Bay and Raffles Place fell slightly, resulting in a drop in the overall occupancy rate in the CBD to 95.2% in Q4 2022.

- With limited supply of quality spaces, despite lower occupancy rates in the quarter, rents rose across most subzones of the office sector in Q4 2022, albeit to various extents. In the CBD, premium rents at Marina Bay and Grade A rents at Raffles Place rose by 1.5% q-o-q. In non-CBD, rents of premium office spaces in Marina Centre and City Hall/Bugis improved by 1.0% and 1.5% q-o-q. Office rents in the decentralised areas rose by 0.2% q-o-q in Q4 2022.

- In 2022, in the CBD, premium rents at Marina Bay and grade A rents at Raffles Place saw 6% and 5% growth, respectively. In non-CBD, prime offices spaces in Marina Centre and City Hall/Bugis saw 2-3% rental growth and in the decentralised sub-market, office rents saw a 1% rental growth over the year.

- Some of the major leasing updates in Q4 2022 include Celanese moving into the redeveloped Hub Synergy Point and Standard Chartered Bank reducing in their office space leased at MBFC Tower 1.

Market Outlook

- The office market saw consistent leasing demand throughout the year despite economic headwinds and recent rounds of layoffs in several firms within the tech industry. We expect the positive momentum to continue going into 2023.

- As an attractive financial hub and one of the world’s best places to do business, Singapore has continued to attract new entrants looking to set up businesses in the Southeast Asian market.

- Given the limited supply of quality office spaces, the office market will likely continue to see leasing demand by firms in the finance and wealth management industries.

- However, with greater office completions slated in 2023 coupled with slowing economic growth, rental growth could moderate. Despite that, rental growth will likely continue into the next year, given that supply remains fairly tight.

- We expect Premium and Grade A office rents to rise by 2-4% and 1-3% respectively in 2023.

GENERAL DISCLOSURE

DISCLAIMER - EDMUND TIE & COMPANY

This report should not be relied upon as a basis for entering into transactions without seeking specific, qualified, professional advice. Whilst facts have been rigorously checked, Edmund Tie & Company can take no responsibility for any damage or loss suffered as a result of any inadvertent inaccuracy within this report. Information contained herein should not, in whole or part, be published, reproduced or referred to without prior approval. Any such reproduction should be credited to Edmund Tie & Company.

© Edmund Tie & Company January 2023

Source: Edmund Tie & Company. Reproduced with permission.

Citibank Disclaimers and Important Notices

DISCLAIMER – CITIBANK

The market data and information herein contained (“Information”) is the product or service of a third party not affiliated to Citibank Singapore Limited (“CSL”) or its related entities. None of the Information represent the opinion of, counsel from, recommendation or endorsement by CSL, its related entities and their respective officers, employees, directors and agents (collectively, the “CSL Group”).

The Information is provided for general information and/or educational purposes only. No part of the Information may be reproduced without the prior written permission of CSL.

NO WARRANTY

The Information is provided “as is”, without warranty of any kind, it has not been independently verified by CSL Group and use of the Information is at your sole risk. The CSL Group shall not be liable and expressly disclaim liability for any error or omission in the content of the Information, or for any actions taken by you or any third party, in reliance thereon. The Information is not guaranteed to be error-free, or to be relied upon for investment purposes, and the CSL Group makes no representation or warranty as to the accuracy, truth, adequacy, timeliness or completeness, fitness for purpose, title, non infringement of third party rights or continued availability of the information.

LIMITATION OF LIABILITY

To the maximum extent permitted by law, the CSL Group shall not be liable for any loss or damage of any kind whatsoever (including, without limitation, any special, consequential, incidental or indirect damages, or damages for loss of profits, business interruption, and any and all forms of loss or damage, regardless of the form of action or the basis of the claim, whether or not foreseeable) arising out of the use of the information (provided in any medium), even if any member of the CSL Group, has been advised of the possibility of such loss or damage.

© 2023 CITIBANK

CITIBANK IS A REGISTERED SERVICE MARK OF CITIGROUP INC. OR CITIBANK, N.A.

CITIBANK SINGAPORE LIMITED. CO REG. NO. 200309485K